Accounting

Anthropology

Archaeology

Art History

Banking

Biology & Life Science

Business

Business Communication

Business Development

Business Ethics

Business Law

Chemistry

Communication

Computer Science

Counseling

Criminal Law

Curriculum & Instruction

Design

Earth Science

Economic

Education

Engineering

Finance

History & Theory

Humanities

Human Resource

International Business

Investments & Securities

Journalism

Law

Management

Marketing

Medicine

Medicine & Health Science

Nursing

Philosophy

Physic

Psychology

Real Estate

Science

Social Science

Sociology

Special Education

Speech

Visual Arts

Question

A bank has a positive repricing gap and estimates that the spread between RSAs and RSLs will move directly with interest rates. If interest rates fall, the bank's overall NII will

A. rise.

B. fall.

C. be unchanged.

D. rise or fall depending on the size of the spread effect relative to the size of the CGAP effect.

Answer

This answer is hidden. It contains 1 characters.

Related questions

Q:

The bank keeps a capital-to-asset ratio of 8%. If the bank does not securitize the mortgages, they will be fully funded with demand deposits that have a reserve requirement of 10%. The demand deposits also have a deposit insurance premium of 0.20 cents per $100 of deposits. If the bank securitizes the mortgages, how much less capital will the bank require? If the savings from not having the required reserves and the deposit insurance premiums could be invested at 5%, what is the dollar opportunity cost of not securitizing?

Q:

What is the total amount of net fee revenue generated from the mortgages over the year?

Q:

A U.S. firm is earning British pounds from its foreign subsidiary. A U.K. firm is earning dollars from its U.S. subsidiary. Neither firm can borrow at a cost-effective rate outside of its home country/currency. What kind of swap could be used to limit the FX risk of both firms and explain the payment flows involved (be specific)?

Q:

Plain vanilla interest rate swaps are exchanges of

A. principle only.

B. interest only.

C. principle and interest.

D. principle and currency.

E. interest rate and currency.

Q:

A _____ position in T-bond futures should be used to hedge falling interest rates and a _____ position in T-bond futures should be used to hedge falling bond prices.

A. long; short

B. long; long

C. short; long

D. short; short

Q:

The price of a bond rises from 98 to par. Even if you do nothing, this would still result in an immediately recognized loss on a _____________ on a bond, and a paper gain on a bond ______________.

A. long forward contract; call option

B. short futures contract; call option

C. call option; put option

D. short futures contract; put option

E. short forward contract; call option

Q:

A bond portfolio manager has a $25 million market value bond portfolio with a 6-year duration. The manager believes interest rates may increase 50 basis points. Which of the following could be used to help limit his risk?

I. Sell the bonds forward.

II. Buy bond futures contracts.

III. Buy call options on the bonds.

IV. Buy put options on the bonds.

A. I only

B. II only

C. I and III only

D. I and IV only

E. II and III only

Q:

A bank has a positive repricing gap and wishes to protect its profits from an unfavorable interest rate move. Purchasing a cap will help limit this bank's interest rate risk.

Q:

A macro hedge is a hedge of a particular asset or liability exposure to a change in a macroeconomic variable.

Q:

Buying a cap is similar to buying a call option on bond prices.

Q:

Figure 22-3 A thrift has an annual CGAP of -$25 million. A credit union has an annual CGAP of +$5 million. The thrift has total assets of $500 million and net income of $7.5 million and the credit union has total assets of $40 million and net income of $0.7 millionCalculate each institution's CGAP as a percent of assets. Based on the gap, which institution's NII is more sensitive to interest rates? Explain.

Q:

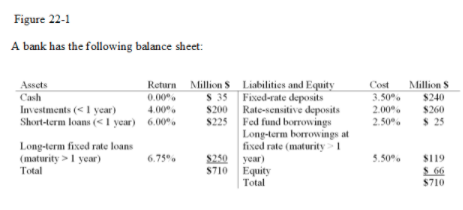

The bank's one-year repricing gap is (Million $)A. $425.B. $285.C. $74.D. $140.E. $66.

Q:

Due to convexity problems, banks are actually better off using the simpler repricing model to manage interest rate risk rather than the duration model.

Q:

The cash flow from the interest a bank receives on a long-term loan that is normally reinvested is called the runoff from the loan.

Q:

If a bank has a negative repricing gap, falling interest rates increase profitability.

Q:

In a bank's three-month maturity bucket, a 30-year ARM with a rate reset in six months would be considered a fixed rate asset, but in its one-year maturity bucket, this ARM would be considered a rate-sensitive asset.

Q:

Why might a bank face abnormal deposit drains?

Q:

Explain the relationship between each of the following ratios and liquidity risk.

a) Loan-to-deposit ratio

b) Borrowed funds to total assets

c) Loan commitments to total assets

Q:

Explain how liquidity risk can lead to insolvency risk.

Q:

In the absence of deposit insurance, a deposit is a _______________ to the bank's assets.A. pro rata claimB. first come/first serve claimC. full pay or no pay claimD. both A and BE. both B and C

Q:

An increasingly positive financing gap can indicate ________________ liquidity risk because it may indicate _______________ deposits and/or rising loan commitments.A. increasing; increasingB. decreasing; decreasingC. increasing; decreasingD. decreasing; increasing

Q:

The BIS recommends that depository institutions do which of the following to realistically measure liquidity risk?I. Construct a maturity ladder of funding requirements over both the short and long run.II. Conduct scenario analyses of the bank's implied liquidity position under different bank and economic conditions.III. Always keep the loan to deposit ratio less than one.A. I onlyB. II onlyC. I and II onlyD. II and III onlyE. I, II, and III

Q:

A bank meets a deposit withdrawal with one of the following alternatives. Which one of the following is an example of using stored liquidity to meet a deposit withdrawal?A. Increase in Euro dollar depositsB. Contacting an investment banker to find new corporate depositsC. Increasing Fed funds borrowedD. Issuance of a negotiable CDE. Selling the bank's holdings of T-bills

Q:

A four-class CMO has Class A, Class B, Class C, and the residual Class Z securities outstanding. Which class has the longest duration?

A. Class A

B. Class B

C. Class C

D. Class Z

E. All have the same duration

Q:

Banks were willing to swap LDC loans for Brady bonds because:

A. Brady bonds carried higher interest rates than the loans.

B. the bonds had variable interest rates.

C. the bonds were marketable and the loans were not.

D. the bonds were uncollateralized.

E. none of the above

Q:

A CMO is a multiclass pass-through that helps investors choose the amount of prepayment risk they will face.

Q:

Under current reserve requirements, bank loan sales with recourse are considered a liability and are subject to reserve requirements.

Q:

Vulture funds specialize in buying distressed loans.

Q:

More than 90% of loan sales are via assignments.

Q:

The buyer of a loan in a participation has a double-risk exposure: one to the borrower and one to the selling bank.